The 2025 tax filing season is officially underway, and American taxpayers are poised to receive what experts are calling the largest tax refunds in U.S. history. With the IRS beginning to accept returns on January 26, millions of households can expect an average refund of approximately $3,200—a staggering $1,000 increase from last year—thanks to landmark tax reforms enacted through the One Big Beautiful Bill Act (OBBBA). For investors and financially savvy individuals, this unprecedented windfall represents not just extra spending money, but a significant opportunity to accelerate wealth building, reduce debt, and secure long-term financial stability.

How Historic Tax Reforms Are Creating Record Refunds

House Ways and Means Committee Chairman Jason Smith (R-Mo.) announced earlier this month that American taxpayers are projected to receive an additional $91 billion in tax refunds this year, with total refunds expected to reach a record-setting $370 billion. "Families can expect an average of $1,000 more in their refund compared to last year," Smith stated in a news release. "For a family with two kids making $73,000, they will have zero tax liability. Bigger refunds mean more money to cover groceries, doctors' bills, school supplies and summer activities."

The tax reforms include several key provisions that directly impact refund amounts: elimination of taxes on tips and overtime, no tax on Social Security benefits, a larger standard deduction, expanded Child Tax Credit, and permanently lower tax rates. Treasury Secretary Scott Bessent told NBC10 Philadelphia that "I think we're going to see $100 [billion]-$150 billion of refunds, which could be between $1,000 and $2,000 per household." President Donald Trump himself declared at a Cabinet meeting in December that this tax filing season is "projected to be the largest tax refund season ever."

Timeline: When You Can Expect Your 2025 Tax Refund

The IRS has established clear timelines for refund processing, though these vary significantly depending on filing method. Electronic filers—which represented 93% of taxpayers last year—typically receive their refunds in less than 21 days. This means a taxpayer who files a Form 1040 on January 26 could receive their refund by February 16, assuming no issues with the return. Paper returns, however, require manual processing by IRS employees and can take 6 to 8 weeks for refund delivery.

Taxpayers who claim the Earned Income Tax Credit (EITC) or Additional Child Tax Credit (ACTC) face additional delays due to fraud prevention measures. By law, the IRS must hold these returns longer to scan for potential errors or misapplied credits. Approximately one-third of EITC claims are paid in error because some taxpayers may not understand whether they qualify. As a result, people who claimed either the EITC or ACTC won't get their refund until March 2 at the earliest.

Why This Refund Season Is Different: Economic Context and Implications

The timing of these larger refunds couldn't be more significant for American households. After years of inflationary pressures that have increased costs for everyday essentials like groceries, housing, and healthcare, these substantial refunds provide much-needed financial relief. Janet Holtzblatt, a senior fellow at the Urban-Brookings Tax Policy Center, noted in a blog post earlier this month that "Taxpayers might want to lower their expectations and prepare for unanswered phone calls to the IRS and delays in tax refunds, given these ingredients for a problem-prone filing season."

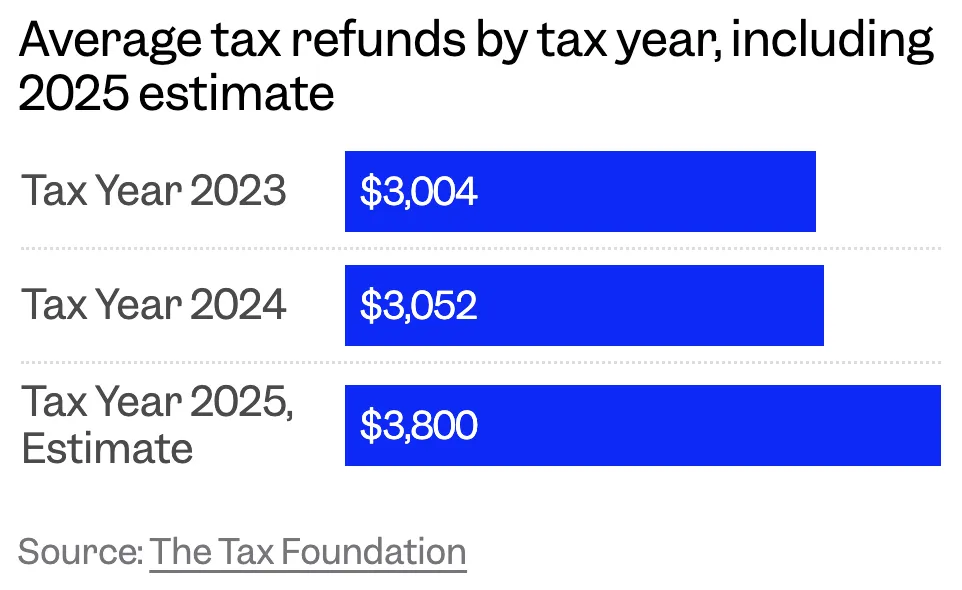

IRS data for the 2025 tax filing season shows the average refund increased to $3,167 as of December—a gain of 0.9% from the 2024 filing season. Over 103.8 million tax refunds were issued in the last tax filing season, representing a 1% decrease from the prior year. The total amount refunded was nearly $329 billion in last year's tax season, essentially unchanged after a 0.1% decrease from the prior year. The overwhelming majority of refunds (94.3 million) were issued by direct deposit, with more than $304 billion disbursed back to taxpayers through this electronic method.

Where Things Stand Now: IRS Tools and Filing Recommendations

The IRS has significantly enhanced its "Where's My Refund?" tool for the 2025 filing season, providing taxpayers with clearer and more detailed updates about their refund status. The tool now offers three key pieces of information: IRS confirmation of receiving a federal tax return, approval of the refund, and the date when the refund will be sent. Taxpayers can typically access information about 24 hours after submitting a current-year return via e-filing, or four weeks after filing a paper return.

To use the "Where's My Refund?" tool, taxpayers need their Social Security or individual taxpayer ID number (ITIN), filing status, and the exact refund amount shown on their return. The app displays one of several statuses: Return Received (IRS has received your return and is processing it), Refund Approved (IRS approved your refund and is preparing to issue it by the date shown), or Refund Sent (IRS sent the refund to your bank or to you in the mail). Financial experts universally recommend filing electronically and selecting direct deposit as the fastest way to receive your refund.

What Happens Next: Smart Investment Strategies for Your Tax Refund

With average refunds approaching $3,200, financial advisors are urging taxpayers to think strategically about how to deploy these funds for maximum long-term benefit. According to Lewis Financial and other wealth management firms, here are the five most effective ways to transform your tax refund into lasting financial security:

1. Eliminate High-Interest Debt: Credit card debt with interest rates of 18-25% represents an immediate negative return on your money. Paying off such debt effectively guarantees a risk-free return equal to the interest rate you're avoiding. This should be the first priority for anyone carrying credit card balances or other high-interest loans.

2. Build or Replenish Your Emergency Fund: Financial experts recommend maintaining 3-6 months' worth of essential living expenses in a readily accessible account. If your emergency fund is underfunded, consider allocating a portion of your refund to this crucial financial buffer. High-yield savings accounts or money market funds currently offer 4-5% returns while maintaining liquidity.

3. Boost Retirement Savings: If you already have a 401(k), consider increasing your contribution by 1-2% and using the refund to "cover the gap" in your budget. For those without an IRA, you can open and fund one with your refund—contributions to traditional IRAs may be tax-deductible, while Roth IRAs offer tax-free growth. The 2025 contribution limits are $7,000 ($8,000 if age 50+).

4. Invest in Taxable Brokerage Accounts: For longer-term goals beyond retirement, consider investing in low-cost index funds or ETFs through a taxable brokerage account. A $3,200 investment in an S&P 500 index fund with an average annual return of 8% would grow to approximately $15,800 in 20 years without additional contributions.

5. Fund Education Savings (529 Plans): These state-sponsored plans offer tax-free growth when used for qualified education expenses. Many states provide additional tax deductions or credits for contributions. With college costs continuing to rise, early funding of 529 plans can significantly reduce future education debt burdens.

The Bottom Line: Key Points Every Investor Should Remember

The 2025 tax season represents a unique financial opportunity for American households. Record-breaking refunds averaging $3,200+ provide a substantial lump sum that can accelerate financial goals when deployed strategically. The most important takeaways: file electronically with direct deposit for fastest processing, track your refund using the enhanced IRS tool, and prioritize debt elimination and retirement savings over discretionary spending. As Treasury Secretary Bessent noted, the timing of the tax cut's enactment last summer didn't give Americans the opportunity to change their withholding for the remainder of 2025, creating these "very large refunds" that can now be strategically invested for long-term wealth building.