Taking on debt has become a common financial strategy for individuals and businesses alike. However, the true cost of debt is more than just the amount borrowed—it includes interest rates, fees, and the broader economic impact it can have on your financial stability. Understanding why debt is so expensive can help you make smarter borrowing decisions and reduce long-term financial risk.

Understanding the True Cost of Debt

The cost of debt encompasses more than just your monthly repayments. It includes interest charges, loan origination fees, and sometimes penalties for early repayment. These added expenses can significantly inflate the total amount you owe over the life of a loan. Understanding these components is crucial for anyone considering borrowing, as even a small percentage increase in interest rates can translate into thousands of dollars over time.

High Interest Rates Inflate Borrowing Costs

One of the most significant factors contributing to the cost of debt is the interest rate. Lenders assign rates based on a borrower’s creditworthiness, length of the loan term, and prevailing economic conditions. When interest rates rise, so does the cost of borrowing. For every additional percentage point, your monthly payment and the total interest paid over the loan’s term increase, making debt more expensive.

Credit Scores and Risk Assessment

Your credit score plays a pivotal role in determining how much you’ll pay to borrow. Lenders view low credit scores as higher risk and charge higher interest rates to compensate. Poor credit history can also lead to loan denial or stricter borrowing terms. Improving your credit score by paying bills on time and reducing other debts can significantly lower the cost of debt.

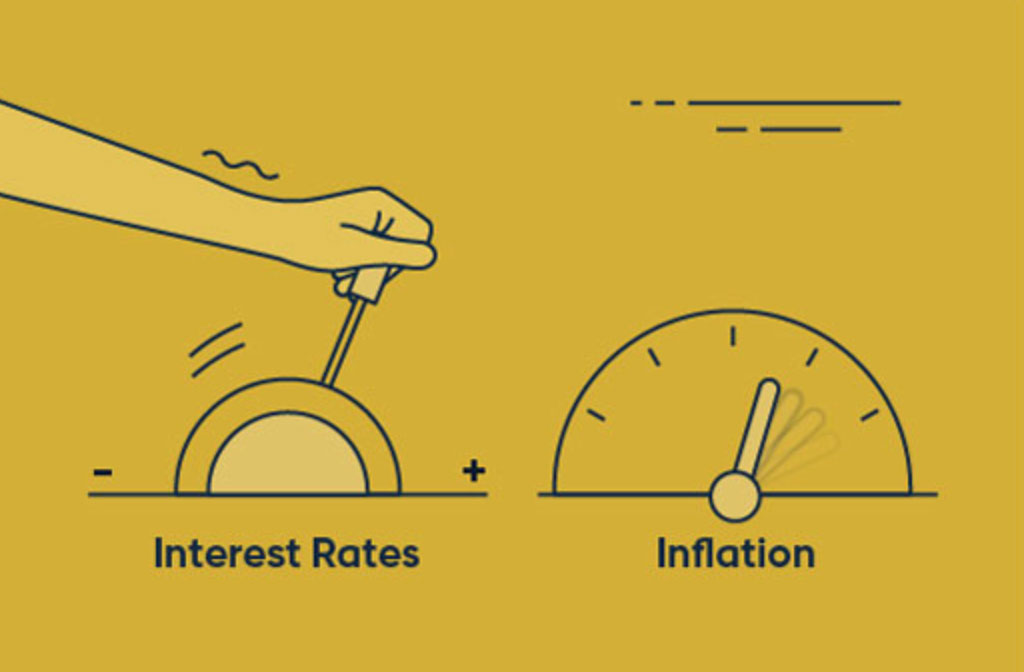

Inflation and Economic Conditions

Economic factors such as inflation and monetary policy directly affect interest rates and, in turn, the cost of debt. When inflation rises, central banks often increase rates to curb spending. This leads to higher loan interest rates, driving up the cost of mortgages, auto loans, and credit cards. Borrowers must understand that their loan costs can fluctuate with economic changes.

Loan Terms and Repayment Periods

The length of your loan also contributes to its overall cost. While longer-term loans may offer lower monthly payments, they often carry higher interest rates or accumulate more interest over time. Conversely, shorter-term loans may have higher payments but lower total interest. Choosing the optimal loan term is essential for controlling the long-term cost of debt.

Hidden Fees and Additional Charges

The true cost of debt often includes hidden charges such as origination fees, processing fees, late payment penalties, and prepayment penalties. These fees can add up quickly and inflate your debt beyond the initial loan amount. Always read the fine print and ask lenders to explain any costs not clearly outlined before taking on new debt.

The Burden of Compounding Debt

For many borrowers, failing to manage existing debts can lead to compounding interest, where interest is added to both the principal and accumulated interest. This cycle increases the total owed rapidly, making it harder to break free from debt. Understanding the importance of timely payments and controlling new borrowing is key to avoiding escalating debt costs.

Strategies to Lower Your Cost of Debt

Reducing the cost of debt starts with improving your credit score, shopping around for better interest rates, and negotiating terms with lenders. Refinancing high-interest loans, choosing shorter repayment periods, and avoiding unnecessary borrowing can help you minimize finance charges. Financial literacy and proactive planning are powerful tools against the high expense of debt.

Debt can be a useful financial tool, but its costs can quickly spiral beyond expectations if not managed wisely. From interest rates and loan terms to economic conditions and personal credit scores, multiple factors influence the final cost of debt. By understanding these variables and taking proactive steps, you can make informed borrowing decisions and reduce the financial strain that debt can impose over time.