Palantir Technologies CEO Alex Karp has made headlines on multiple fronts in recent months, creating a complex picture for investors in the high-flying AI stock. From selling over $50 million in company shares to warning that artificial intelligence "will destroy humanities jobs," while simultaneously reporting record-breaking revenue growth of 70%, Karp's actions and statements have sent mixed signals to the market. As Palantir stock (PLTR) continues its volatile ride—surging 148% in 2025 before facing criticism from prominent short-seller Michael Burry—investors are grappling with what these developments mean for one of the most debated companies in the AI space.

Alex Karp's $50 Million Stock Sale: What Investors Need to Know

In May 2025, securities filings revealed that Palantir CEO Alex Karp sold more than $50 million worth of company shares, liquidating approximately 390,417 shares at prices between $128 and $131 per share. The sales, executed on May 20 and 21, represented vesting stock that Karp had acquired through previous compensation packages. While significant, these transactions differed from the massive stock sales by Palantir executives in previous years, with Sherwood News reporting they were primarily for "tax reasons" rather than a fundamental shift in confidence.

This wasn't Karp's only stock sale in recent months. Additional filings showed he sold another $66 million in Palantir stock in November 2025 amid a broader downturn in AI-related tech stocks. Despite these sales, Karp still maintains significant ownership in the company he helped found, holding approximately 6.4 million Class A shares worth nearly $800 million at current prices. For investors, executive stock sales always warrant attention, but context matters—these were planned transactions of vesting shares rather than open market sales indicating immediate concern about the company's prospects.

From Boom to Criticism: Palantir's Rollercoaster 2025

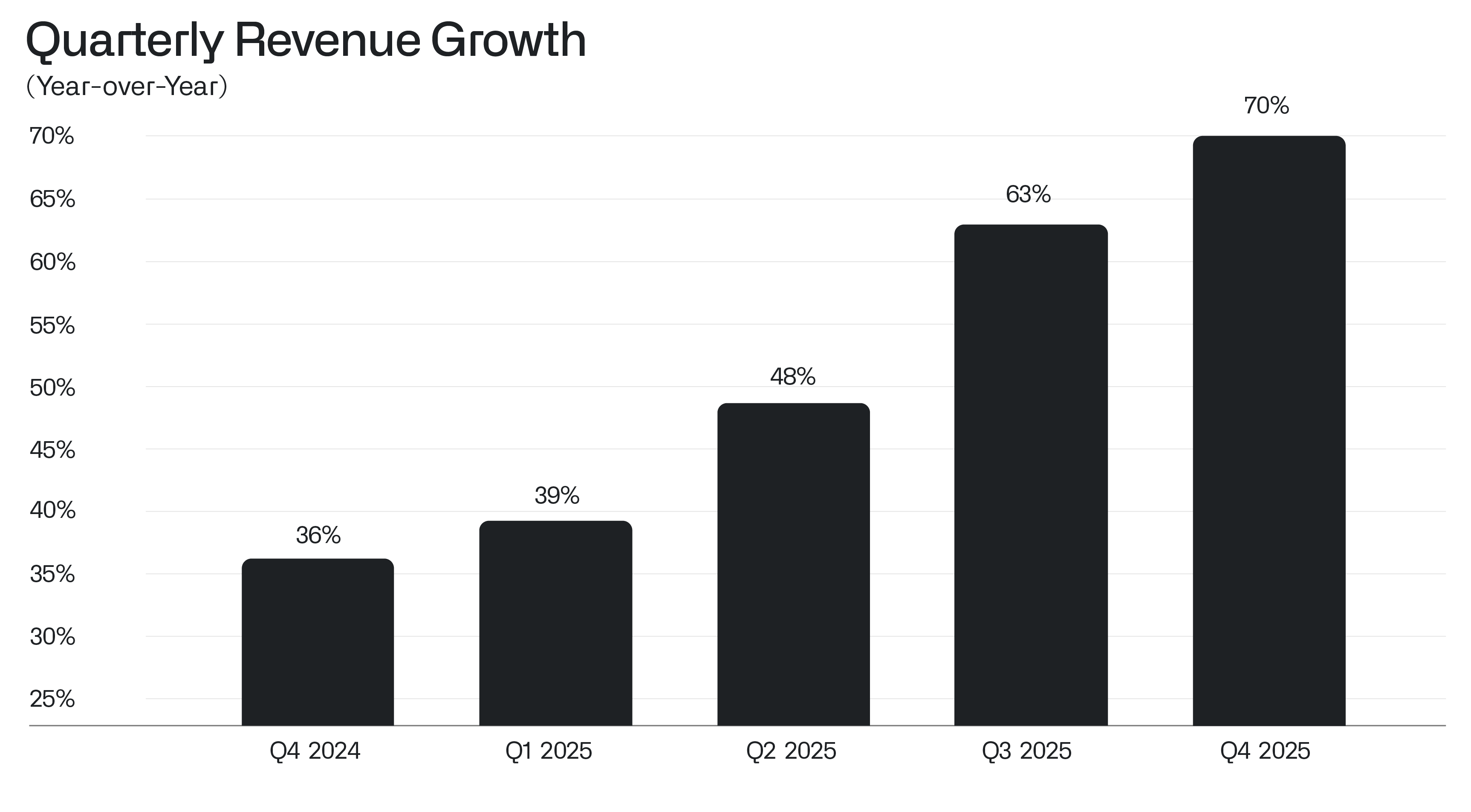

The past year has been a wild ride for Palantir shareholders. The stock surged an astonishing 148% in 2025, driven by booming demand for the company's AI platforms and significant military contract wins, including a $30 million deal with U.S. Immigration and Customs Enforcement to build the "ImmigrationOS" surveillance platform. This growth culminated in February 2026 when Palantir reported fourth-quarter revenue of $1.4 billion—a 70% year-over-year increase that crushed Wall Street expectations.

However, the celebration was short-lived. In April 2026, "Big Short" investor Michael Burry delivered a scathing critique of Palantir, writing in a since-deleted social media post that Anthropic was "eating Palantir's lunch" in enterprise AI. Burry cited data from corporate spend tracker Ramp showing Anthropic capturing "73% of all new enterprise spending" and argued that Palantir was essentially a "low-margin consulting business" rather than a true AI company. The criticism hit hard: Palantir stock dropped 8% in a single day as investors digested Burry's analysis that the company "has no real AI software of its own" and depends on embedding engineers in client offices rather than selling scalable software.

Why Karp's AI Warning Matters for Investors

Perhaps the most surprising development came from Karp himself during the World Economic Forum in Davos, where he delivered a stark warning about AI's impact on the job market. "It will destroy humanities jobs," Karp stated bluntly when asked how AI would affect employment. He elaborated that people with elite humanities degrees would find their skills devalued, while those with vocational training would thrive in the new economy.

For Palantir investors, Karp's comments reveal several important insights about the company's strategy and the broader AI market. First, they highlight Palantir's focus on practical, vocational applications of AI rather than theoretical research—aligning with the company's emphasis on government and industrial clients. Second, they underscore the disruptive nature of the technology Palantir is selling, which creates both opportunities and risks. Finally, Karp's personal background (he holds a PhD in philosophy from Stanford) adds weight to his warning, suggesting he understands both sides of the humanities-versus-technology divide.

Where Palantir Stands After Q4 Earnings Beat

Despite the controversies and criticisms, Palantir's fundamental business performance remains exceptionally strong. The company's fourth-quarter results were nothing short of spectacular: $1.4 billion in revenue represented not just 70% year-over-year growth but also 19% quarter-over-quarter acceleration. Even more impressive was the U.S. commercial revenue growth of 137%, reaching $507 million and demonstrating that Palantir is successfully expanding beyond its traditional government contracting base.

The company's "Rule of 40" score—a key metric for software companies that combines growth and profitability—reached an extraordinary 127%, far exceeding the 40% threshold that indicates healthy balance. Palantir also issued optimistic guidance for 2026, forecasting approximately $7.2 billion in full-year revenue representing 61% year-over-year growth. These numbers help explain why, despite Burry's criticism and Karp's stock sales, many analysts remain bullish on Palantir's long-term prospects in the AI revolution.

The Road Ahead for Palantir and AI Stocks

Looking forward, Palantir faces both significant opportunities and substantial challenges. On the positive side, the company continues to win major government contracts, including recent extensions with defense and intelligence agencies that provide stable, recurring revenue. The commercial business is growing at triple-digit rates, suggesting Palantir's AI platforms are gaining traction in the private sector. And with AI adoption still in its early innings across most industries, the total addressable market continues to expand.

However, competition is intensifying. Burry's criticism about Anthropic highlights the threat from pure-play AI companies that offer more standardized, API-driven solutions compared to Palantir's customized approach. Valuation remains a concern—even after recent declines, Palantir trades at approximately 142 times expected earnings, making it the third-most expensive stock in the S&P 500. And ongoing scrutiny of executive stock sales, while arguably routine, creates periodic negative headlines that can pressure the stock in the short term.

Key Takeaways for Investors

The recent developments around Alex Karp and Palantir offer several important lessons for investors navigating the volatile AI sector. First, executive stock sales should be evaluated in context—planned sales of vesting shares differ fundamentally from emergency liquidations. Second, strong fundamental performance can outweigh even high-profile criticism, as demonstrated by Palantir's stock recovery following its exceptional earnings report. Third, the AI revolution is creating winners and losers across the job market, with companies like Palantir positioned to benefit from the shift toward vocational, practical applications of artificial intelligence. Finally, in a sector characterized by extreme valuations and rapid change, maintaining a balanced perspective—acknowledging both the transformative potential and the legitimate risks—remains essential for long-term investment success.