Mortgage rates have entered a new phase of stability after a volatile year, with December 2024 rates settling between 6.875% and 7.125% following the Federal Reserve's September and November rate cuts. This cooling period represents a two-year low for borrowing costs, yet the housing market continues to face headwinds as elevated rates keep affordability challenging for many homebuyers. For real estate investors, understanding where rates are headed and how they impact market dynamics is crucial for making informed decisions in the coming year.

The December Rate Reality: What the Numbers Show

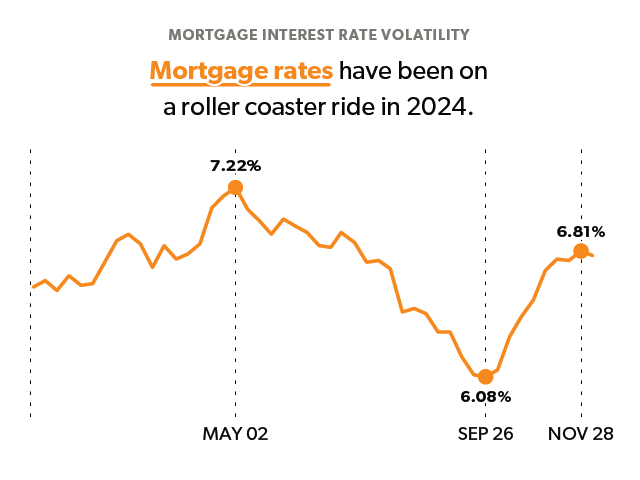

The Federal Reserve's dual rate cuts in September and November 2024 created a ripple effect through the mortgage market, pushing 30-year fixed rates down to levels not seen since late 2022. According to CBS News, experts like Aaron Gordon, a branch manager and senior mortgage loan officer at Guild Mortgage, expect rates to "stay around 6.875% to 7.125% in December." This represents a significant cooling from the peak above 8% seen earlier in 2024, but still remains substantially higher than the sub-3% rates that characterized the pandemic-era housing boom.

The impact of these rate movements is already visible in market data. Melissa Cohn, regional vice president of William Raveis Mortgage, notes that "mortgage rates are likely to be stable in December as the markets continue to digest the planned new policies from the President-elect." This stability comes after a period of rapid adjustment, with mortgage rates plunging to a two-year low in anticipation of the Fed's first cut in years, only to settle into their current range as economic uncertainties persist.

From September to December: The Timeline of Rate Movements

The path to December's rate environment unfolded through a series of calculated Federal Reserve moves and market reactions. In September 2024, the Fed implemented its first rate cut after months of holding steady, sparking immediate optimism in the mortgage market. November brought another 25-basis-point reduction, further fueling expectations of declining borrowing costs. However, as Cameron Burskey, senior partner and managing director of retirement security at Cornerstone Financial Services, explains, "significant decreases are unlikely, as most forecasts suggest that the 30-year fixed rate will remain above 6% until 2025."

December's stability represents a pause in this downward trajectory, with markets now waiting for clearer signals about inflation control and economic direction. The seasonal slowdown in housing activity, combined with typical year-end market quietness, has created a holding pattern that experts believe will continue into early 2025. This timeline of gradual reduction followed by stabilization sets the stage for what investors can expect in the coming months.

Why Mortgage Rates Matter for Real Estate Investors

For investors, the current mortgage rate environment presents both challenges and opportunities. Elevated rates continue to suppress transaction volumes, with Realtor.com reporting that December 2024 was "the slowest December since 2019 and the slowest month in nearly two years." This slowdown creates pressure on sellers and may present buying opportunities for investors with available capital. However, the same high borrowing costs that reduce competition also increase carrying costs for investment properties, requiring careful financial modeling.

The Federal Reserve's influence on mortgage rates operates through complex channels. While the Fed doesn't directly set mortgage rates, its benchmark rate decisions influence the 10-year Treasury yields that mortgage rates closely track. As Bankrate explains, "While the Fed cut the rate three times at the end of 2024, mortgage rates remained relatively high, and even increased. That's because fixed-rate mortgages are priced off of the 10-year Treasury yield, which is influenced by many factors beyond the Fed's policy rate." This disconnect means investors must monitor broader economic indicators, not just Fed announcements, to anticipate rate movements.

Where Things Stand Now: December's Market Reality

The current housing market reflects the tension between improved rate conditions and persistent affordability challenges. Fannie Mae's Home Purchase Sentiment Index decreased 1.9 points in December to 73.1, though it remains substantially higher than year-ago levels. A telling statistic: 42% of consumers expect mortgage rates to decline over the next 12 months, down from 45% in November but meaningfully improved compared to last December's 31%. This cautious optimism suggests that while buyers recognize improvement, they remain wary of expecting rapid declines.

Market activity data reinforces this mixed picture. Pending home sales broke a four-month winning streak by ticking downward 5.5% in December, according to Rate.com. Inventory levels also declined 8.6% month-over-month from November, reaching their lowest level since June. These numbers indicate that while lower rates have prevented a complete market freeze, they haven't been sufficient to spark the kind of robust activity that would signal a true market recovery.

The Road Ahead: What Investors Should Expect in 2025

Looking forward, experts project a gradual easing of mortgage rates through 2025 and 2026. Freddie Mac forecasts that "mortgage rates will decline over 2025, but very gradually," with expectations that rates will average around 6.3% by the end of 2025 and 6.2% by 2026. This slow descent reflects the Fed's cautious approach to further rate cuts amid ongoing inflation concerns and economic uncertainties.

For investors, this outlook suggests several strategic considerations. First, the window of relatively higher rates may persist through much of 2025, favoring cash buyers and those with access to alternative financing. Second, the gradual nature of expected declines means that timing the market perfectly will be challenging—consistent investment approaches may prove more effective than trying to catch the absolute bottom. Finally, regional variations will become increasingly important as national trends mask local market dynamics that may present specific opportunities.

Key Takeaways for Smart Investing in Today's Market

The current mortgage rate environment demands a balanced approach from real estate investors. While rates have cooled from their peaks, they remain elevated by recent historical standards, affecting both acquisition costs and potential returns. Successful investors will focus on properties with strong fundamentals that can withstand potential rate fluctuations, maintain conservative leverage ratios to manage higher borrowing costs, and stay informed about both Federal Reserve policy and broader economic trends that influence mortgage markets. With careful planning and strategic execution, today's market conditions can still yield attractive opportunities for those who understand how to navigate the complexities of mortgage rate dynamics.