The Federal Reserve delivered a cautious but revealing message to investors this week, holding interest rates steady for the second consecutive meeting while signaling a divided path forward. In a pivotal 11-1 vote on March 18, 2026, the Federal Open Market Committee (FOMC) maintained the benchmark federal funds rate at 3.5%-3.75%, but the real story emerged from the updated economic projections and surprising commentary from one of the Fed's most influential voices. With inflation forecasts revised higher and the "dot plot" showing just one expected rate cut this year, investors now face a complex landscape of diverging Fed views, economic uncertainties, and strategic decisions that could define portfolio performance for the remainder of the decade.

The Fed's Steady Hand: What Actually Happened at the March Meeting

After three consecutive 25 basis point cuts in September, October, and December of 2025 brought the federal funds rate down from its peak, the Federal Reserve has now paused for two straight meetings. The March 18 decision saw the FOMC vote 11-1 to keep rates in the 3.5%-3.75% range, with the lone dissent coming from Governor Stephen Miran, who preferred an immediate quarter-point reduction. This "steady as she goes" approach reflects the central bank's delicate balancing act: acknowledging softening economic indicators while remaining vigilant about persistent inflationary pressures.

Fed Chair Jerome Powell emphasized the committee's data-dependent stance, noting that "the forecast is that we will be making some progress on inflation, not as much as we had hoped, but some progress." The decision comes amid growing uncertainty from the ongoing conflict in Iran, which has pushed oil prices toward $100 per barrel and complicated the inflation outlook. Powell acknowledged the geopolitical risks but maintained that it's "too soon to know" the full economic impact, leaving investors to navigate a foggy policy landscape with limited forward guidance.

Reading Between the Dots: What the Fed's Projections Reveal

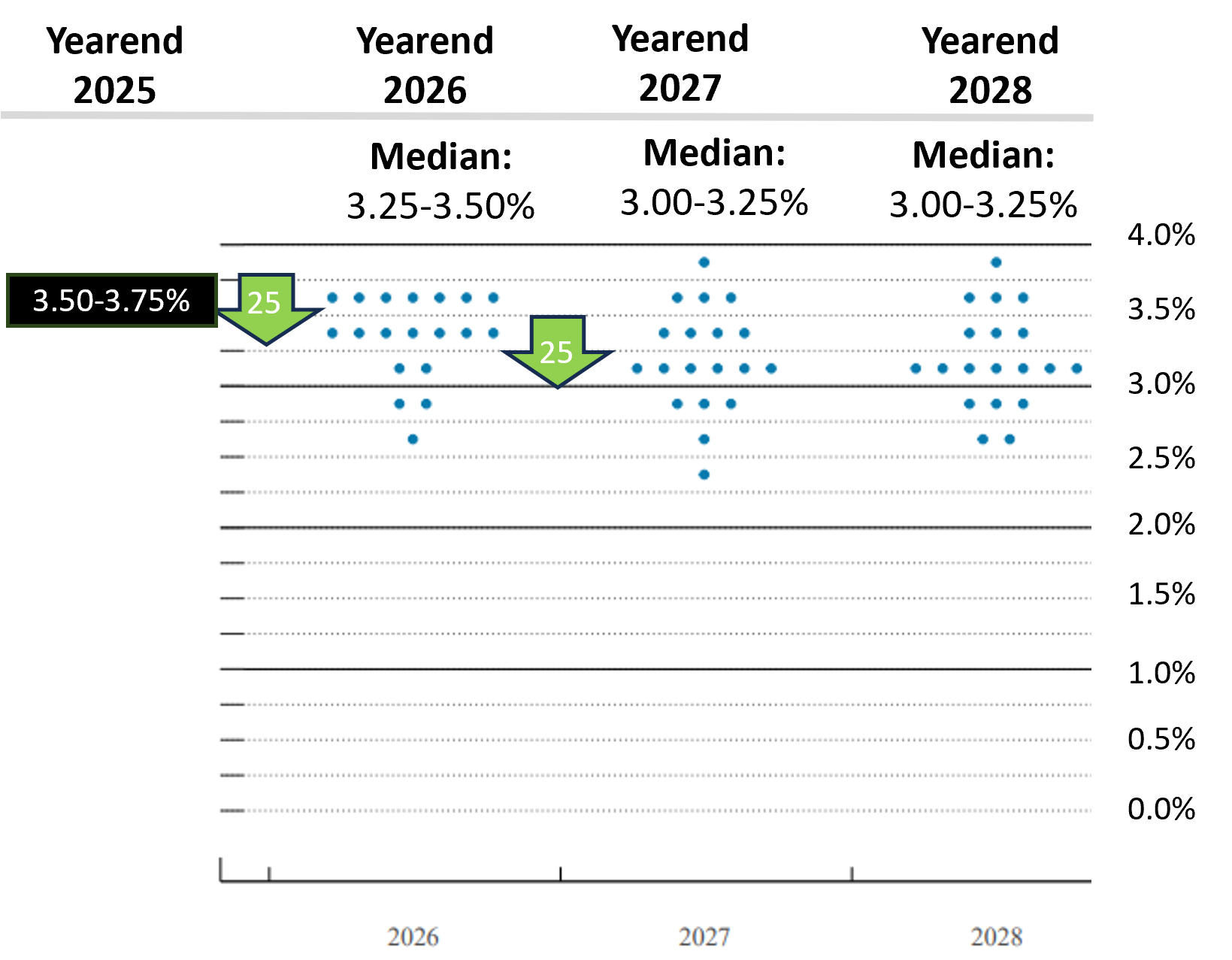

The most closely watched element of any FOMC meeting isn't the immediate rate decision—it's the Summary of Economic Projections, commonly known as the "dot plot." This chart of anonymous policymaker forecasts provides critical insight into where the Fed thinks it's headed, and the March 2026 edition tells a story of cautious optimism tempered by rising inflation concerns. The median projection shows just one 25 basis point cut in 2026, bringing the year-end target to 3.4%, followed by another single cut in 2027 to 3.1%.

What's particularly revealing in the latest dot plot is the narrowing consensus among policymakers. Fourteen of the nineteen FOMC participants now project either no cuts or just one cut in 2026—a significant consolidation from the wider distribution seen in December 2025. This clustering suggests that despite public divisions, more Fed officials are converging around a "higher for longer" mentality. The inflation forecast for 2026 was revised upward to 2.7% from December's 2.5% projection, while economic growth estimates were also boosted slightly, painting a picture of resilient but still-too-hot inflation.

The Bowman Bombshell: Why One Fed Official Sees Three Cuts Coming

Just two days after the FOMC decision, financial markets received a jolt from an unlikely source: Federal Reserve Vice Chair for Supervision Michelle Bowman. In a March 20 interview with Fox Business, Bowman—historically considered one of the more hawkish members of the committee—revealed she has "penciled in three rate cuts before the end of 2026." This stunning admission contradicts the official median projection of just one cut and exposes deep internal divisions about the appropriate policy path.

"I'm still concerned about the job market," Bowman explained. "I want to see a little bit of recovery there. But, of course, I've written three cuts in for before the end of 2026 to hopefully support the labor market." Her comments suggest that some Fed officials are increasingly worried about softening employment data and are willing to prioritize labor market support over inflation concerns. For investors, Bowman's revelation serves as both a warning and an opportunity: the Fed's public unity may be thinner than it appears, and unexpected policy shifts could emerge if economic conditions deteriorate more rapidly than the median forecast anticipates.

Timeline of Tension: How We Got Here and Where We Might Be Heading

The current Fed stance represents the latest chapter in a multi-year monetary policy saga that began with aggressive rate hikes to combat post-pandemic inflation, transitioned to a cutting cycle in late 2025, and has now entered a "wait and see" phase. Understanding this chronology is essential for positioning investment portfolios in 2026 and beyond. The Fed's September 2025 meeting marked the pivot point, with the first of three consecutive cuts that brought rates down from 4.25%-4.5% to the current 3.5%-3.75% range by year's end.

That easing cycle was predicated on declining inflation and concerns about economic momentum, but 2026 has presented new challenges: resurgent energy prices due to Middle East conflicts, sticky service-sector inflation, and mixed labor market signals. The March decision essentially presses pause on the cutting cycle while the Fed assesses whether these are temporary headwinds or longer-term obstacles. Looking ahead, the trajectory will depend on three key variables: monthly inflation data, employment reports, and geopolitical developments affecting commodity prices.

Investment Implications: How to Position Your Portfolio Now

For investors, the Fed's current stance creates both challenges and opportunities across asset classes. The "higher for longer" interest rate environment suggests that cash and short-term fixed income instruments will continue to offer attractive yields, potentially reaching 4-5% on high-quality money market funds and Treasury bills. This provides a solid foundation for conservative investors and creates a meaningful hurdle rate for riskier assets. However, the divergence between the official Fed projection and Bowman's more dovish outlook introduces uncertainty that savvy investors can exploit.

In the equity markets, the Fed's pause typically benefits sectors less sensitive to interest rates while putting pressure on growth stocks that rely on future earnings discounted at lower rates. Value-oriented sectors like energy, financials, and consumer staples may outperform in this environment, particularly if inflation remains stubborn. For bond investors, the flattening yield curve suggests that intermediate-term Treasuries (5-7 years) offer the best risk-reward balance, providing decent yield while maintaining flexibility if rates do decline later this year or early next.

What History Tells Us About Fed Pauses and Market Performance

Historical analysis of similar Fed policy pauses reveals important patterns for today's investors. Since 1990, there have been six distinct periods where the Federal Reserve maintained interest rates unchanged for at least three consecutive meetings after a cutting cycle. In five of those six instances, the S&P 500 posted positive returns over the subsequent 12 months, with average gains of 11.2%. However, the magnitude and leadership of those gains varied significantly based on what triggered the pause and how long it lasted.

The most relevant historical parallel may be the 2006-2007 period, when the Fed paused after raising rates to combat inflation, only to be forced into emergency cuts as financial conditions deteriorated. While today's economic backdrop differs in important ways, the lesson remains: Fed pauses often precede significant market moves, but the direction depends on whether the pause reflects confidence in a soft landing or blindness to gathering storms. The key differentiator this time may be the unprecedented level of public disagreement among Fed officials, which could either signal healthy debate or institutional uncertainty.

The Bottom Line: Key Takeaways for Strategic Investors

Navigating the current Fed policy landscape requires balancing several competing realities. First, recognize that the official projection of just one 2026 rate cut represents the median view, not a consensus. Second, understand that geopolitical risks, particularly surrounding energy prices, could force the Fed's hand in either direction. Third, maintain flexibility in your portfolio allocation, as the divergence between market expectations and Fed projections creates potential for volatility and opportunity.

Most importantly, remember that successful investing in uncertain times isn't about predicting the Fed's exact moves—it's about positioning your portfolio to withstand multiple possible outcomes. Building resilience through diversification, maintaining adequate liquidity, and focusing on quality assets with sustainable cash flows will serve investors better than betting on any single interest rate path. The Fed may be divided on the details, but your investment strategy doesn't need to be: clarity about your personal financial goals, risk tolerance, and time horizon remains the surest guide through today's complex monetary policy landscape.